The Macroeconomic Trends of the Caucasus

photo credit: Mike Cummings/Yale News

Since the outbreak of the pandemic until the Russia-Ukraine war, economic situation across the South Caucasus was unfavorable. On top of the pandemic, the region withstood several negative shocks. However, Russia-Ukraine war turned out to be beneficial for the region’s economy.

The picture in terms of price dynamics was completely different. Simultaneously with high economic growth, the region was affected by the double-digit inflation.

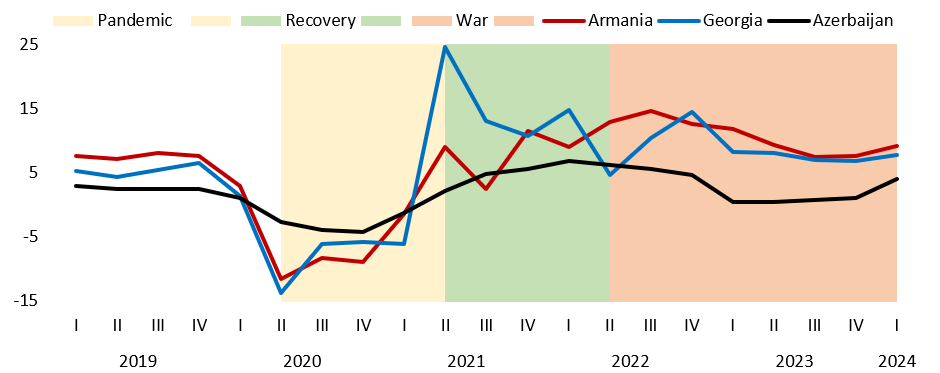

Economic Growth

The first in the region happened as early as in March 2020 when collapse of the alliance between Russia and Saudi Arabia was followed by immediate plummeting of oil prices. Plunging prices and reduced consumption negatively affects the region, because trade partners of Georgia and Azerbaijan, as well as Azerbaijan itself, are oil-exporter countries.

The economies of the South Caucasus were still reeling from the negative shock of oil price drop when the “Great Lockdown” started. The governments curbed activities because of the pandemic that led to the global economy shrinking by 3.1%. Similar processes were unleashed in the South Caucasus, because governments of all three countries implemented lockdowns and restrictions. This caused a sharp contraction of the economy and worsening of the population’s socio-economic situation.

On 27 September 2020 a war broke out between Armenia and Azerbaijan, which ended on 10 November, after Azerbaijan’s military restored control over six regions and President of Azerbaijan, Prime Minister of Armenia and President of Russia signed a trilateral agreement. Apparently, the war negatively affected the entire region, but it was particularly devastating for Armenia that lost the war. In 2020, Armenia’s economy shrank by 7.2% whereas economic decline was 4.2% in the case of Azerbaijan.

Figure 1: Economic Growth Rate of the South Caucasus Nations

Source: National Statistics Offices

After a troublesome 2020 for the region, the following 2021 turned out to be the year of rapid recovery. While in 2020, the economy of the Caucasus decreased by 5.5%, in 2021 economic growth reached 7.8%. As a result, size of the economy exceeded the pre-pandemic economy by 0.7%. The recovery of the Caucasus economy was largely attributable to high economic growth rate in Georgia. In 2021, Georgia’s economy increased by 10.4% and surpassed the size of pre-pandemic economy by 2.9%.

The quick recovery of the region’s economic situation was further abetted by Russia-Ukraine war. In this case, war’s impact on the region’s economy was positive. Migration processes that started as a result of international sanctions imposed on Russia which was later augmented by announcement of the “partial mobilization” led to influx of human capital and therefore remittances from Russia. In turn, remittances stimulate local consumption and is positively reflected on the economy. As a result, after rapid post-pandemic recovery, high economic growth was maintained in Armenia and Georgia.

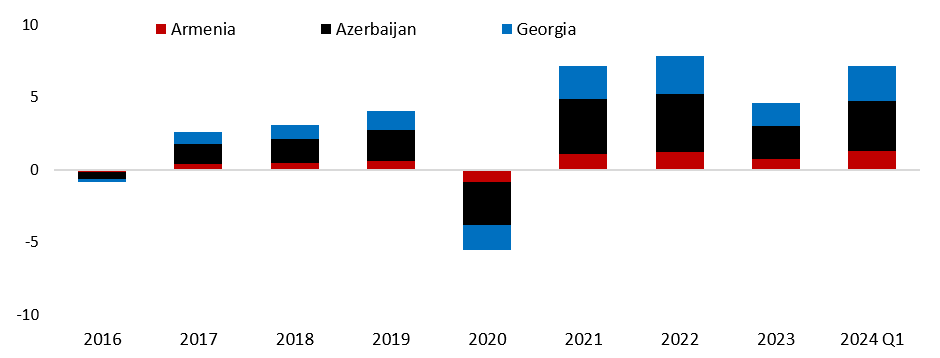

Figure 2: Economic Growth Rate of Caucasus Economies and Contribution by Countries %, P.P

Source: National Statistics Offices ; author’s calculations

However, financial flows slowed down in the next year. For instance, net remittances from Russia in 2023 amounted to USD 1,482.8 million which as compared to the previous year’s figure was 26.8% less. In the same period, total remittances to Armenia dropped by 30.9%. All of these were reflected on the region’s economic growth rate. In 2022, Caucasus economy increased by 7.8% whereas in 2023 by merely 4.6%.

As compared to the region’s countries, Armenia had a relatively higher growth with real gross domestic product increasing by 9.8%. In the same period, Georgia’s economic growth rate amounted to 7.5% whereas in case of Azerbaijan it was 1.1%. The low figure for Azerbaijan was attributable to the oil and gas industry which is a major economic sector of the country. Despite being considered one of the alternatives to provide energy to Europe, the energy sector in Azerbaijan has in fact slowed down. Extraction of raw oil as well as gas sector decreased by 2.4% in 2022 whereas in 2023 drop was 2.8%. At the end of the previous year, this industry is 11% less as compared to the pre-pandemic period. This is precipitated by natural decline in oil extraction at Azeri-Chirag-Gunashli oilfields.

The pace of human and financial flows from Russia is lower this year, although regional economic growth remains at a high level. In the first quarter of 2024, economy of the Caucasus increased by 7.1% whereas as compared to the same period of the previous year, it was 5.3%.

In this period, economic expansion rate in Georgia and Armenia is slower as compared to the same period of the previous year, albeit it increased sharply in Azerbaijan. As of the first quarter of 2024, Armenia’s total GDP growth rate is 9.2% whereas in the same period of 2023 it was 11.8%. In Georgia, economic growth rate in the first quarter of 2023 was 8.2% whereas according to preliminary data it will be 7.8% in the same period of this year. However, in Azerbaijan, economy grew by 4% in the first quarter whereas growth rate in the same period of the previous year was merely 0.4%.

Price Growth

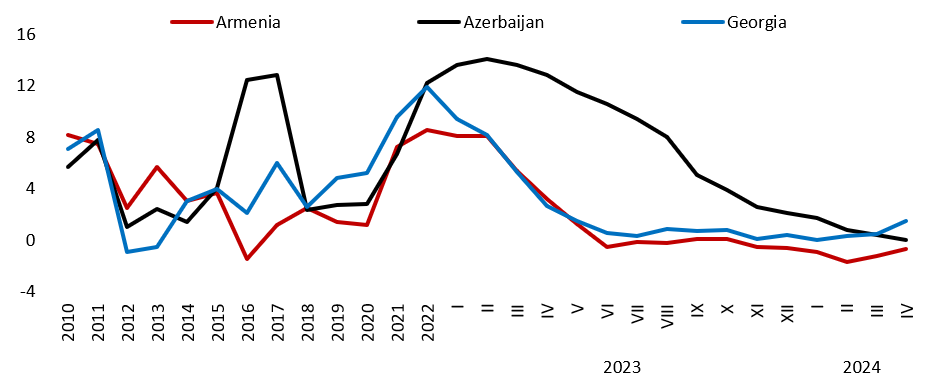

Another important indicator of a macroeconomic situation is inflation which measured by changes in consumer price index. In the abovementioned period inflation too, was high which was preceded by monetary easing launched prior to the pandemic. In 2020, Central Banks started massive monetary easing. In the next year, inflation rate accelerated and reached double-digits in all three countries. In this period, Azerbaijan recorded the highest inflation rate whereas it was the lowest in Armenia.

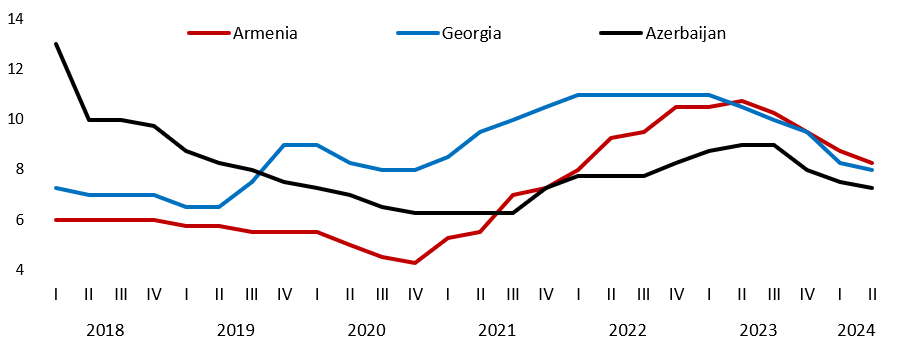

Figure 3: Monetary Policy Rate of the Caucasus Countries by the End of Period, %

Source: Central Banks

In all three countries of the Caucasus, refinancing rate, which is the price commercial banks pay to receive short-term monetary resources from Central Bank, is used as a key monetary policy instrument. An increase in the refinancing rate makes these resources more expensive, which reduces monetary emission rate, whereas cutting the rate has the opposite effect. Therefore, reduction of refinancing rate affects inflation rate.

Since 2018, Azerbaijan’s Central Bank has been actively cutting monetary policy rate. Over the course of two years, the Central Bank decreased refinancing rate from 13% to 7.5% and this trend of reduction continued in the next year. At the end of 2020, Azerbaijani Central Bank’s monetary policy rate was already 6.25%. This led to inflation growth which peaked in January 2023, reaching 14.1%.

Georgia’s National Bank in 2018-2019, initially pursued easing of monetary policy but switched to tightening as early as from the second half of 2019. At the end of 2019, refinancing rate has already increased from 6.5% to 9%. The reason behind this was accelerated inflation and expected sharp price growth for the subsequent period. Despite inflationary background, in 2020, Georgia’s National Bank renewed its monetary easing policy, cutting the refinancing rate from 9% to 8%. In addition, the National Bank also robustly used supervising and other instruments for easing of monetary policy. As a result, it turned out that through this easing policy, the National Bank rejected its principal goal and deviated from its monetary policy rule, because at time of policy change, consumer price growth was around 7% and according to National Bank’s assessment, it was expected that inflation would be higher than the target figure of 3%.

As a result of Georgia’s National Bank’s expansionary monetary policy, consumer price growth rate further accelerated whereas inflation peaked at 13.9% in December 2021. For the 1.5 years, annual growth of rate consumer prices remained in double-digits, and over four years it stayed above target figure.

Figure 4: Changes in Consumer Price Index Across the Caucasus Countries, %

Source: National Statistics Offices

Inflation in Armenia was also above target figure, but to a lesser extent and for a shorter time as compared to Georgia and Azerbaijan.

Armenia’s Central Bank started to ease monetary policy since 2019. At the end of that year, refinancing rate was cut from 6% to 5.5% whereas at the end of 2020 it was already slashed further to 4.25%. As opposed to Georgia and Azerbaijan, monetary easing in Armenia was implemented amid lower inflation. Average annual inflation for 2019 was 1.4% and for 2020 – 1.2%. This is two times and four times less as compared to Georgia’s and Azerbaijan’s figures, respectively, in the same period.

In Armenia too, monetary policy easing was followed by accelerated inflation from 2021. Average annual consumer price growth in 2021 was 7.2% on average. Inflation increased further in the next year and reached double-digit 10.3% in June 2022, then returning to single-digit growth rate from the very next month. Therefore, in contrast to other countries of the Caucasus, the consumer price growth rate in Armenia was in double digits for only one month.

Armenia was among the first to initiate monetary tightening. In early 2021, the refinancing rate increased from 4.25% to 5.25%, and this upward trend continued intensively through the first half of 2023. By the end of the second quarter of 2023, Armenia's refinancing rate had reached 10.75%, coinciding with the first decrease in the consumer price growth rate and a shift towards deflation. Currently, Armenia's inflation rate stands at 0.3%, with the Central Bank's monetary policy rate set at 8.25%.

Around the same time, Georgia also began to increase its refinancing rate, albeit at a slower pace. From the first quarter of 2021 to the corresponding period in 2022, the refinancing rate rose from 8% to 10%. Subsequently, this rate remained unchanged for the next year. Later, the National Bank pursued a sharp easing of monetary policy, achieved not only through adjustments in the refinancing rate but also through extensive foreign exchange interventions. Currently, Georgia's policy rate stands at 8%, and inflation hovers around 2%.

Azerbaijan, in contrast, initially hesitated to tighten its monetary policy, leading to delayed inflation slowdown. By the end of 2021, Azerbaijan's Central Bank began to increase the refinancing rate from 6.25%, reaching 9% by the second quarter of 2023. Currently, consumer price changes in Azerbaijan are close to zero, with the refinancing rate set at 7.25%.

***

Since 2020, the South Caucasus has experienced several shocks, including the oil price crash, extensive economic activity restrictions due to the pandemic, the Karabakh war, and Russia's large-scale invasion of Ukraine. The first three events had a negative impact on the region's economy, resulting in economic contraction. However, subsequent periods saw rapid economic recovery. The Russia-Ukraine war unexpectedly benefitted the Caucasus by driving an influx of human and financial capital from Russia, which proved pivotal in achieving high economic growth rates.

Together with the robust economic growth, the region has also faced significant inflation. When governments restricted economic activity during the pandemic, Central Banks responded with extensive monetary easing, which typically has a delayed effect on prices. Double-digit inflation in the region’s countries turned out to be the result of that policy.

Currently, consumer price growth rate across the Caucasus countries have been significantly slowed down. At the time, relatively high economic growth still continues. Therefore, taking into account both of these parameters, currently region’s macroeconomic situation is better as compared to the previous period.

See the attached file for the entire document with relevant sources, links and explanations.