Credibility of the National Bank

Amidst the Great Inflation, which started in the 1970s, Paul Volcker, chairman of the Federal Reserve System (1979-1987), stated that "to break the [inflation] cycle… we must have a credible and disciplined monetary policy". Another chairman of the Federal Reserve System (2006-2014) and Nobel Prize winner (2022), Ben Bernanke also endorsed the ethos of Mr Bernanke in his series of lectures about the history of the Federal Reserve System – the institution which acts as a central bank and whose principal function is to ensure price stability.

Central Bank pursues exclusively monetary policy. In the case of Georgia, a constitutional body – the National Bank of Georgia- is vested with such authority, exercising a far-reaching power. In particular, the National Bank of Georgia affects each individual who uses Lari – legal tender emitted by the National Bank under uncontested monopoly. Therefore, the National Bank's actions are reflected in Lari's purchasing power. Another critical factor is that the National Bank controls the activities of commercial banks as part of supporting the financial sector's stability. Among other things, this includes the authority of direct interference in a commercial bank's management. Central Bank is the institution that wields broad and flexible instruments to interfere in an economy.

Central Bank is an institution independent from the executive branch of government, generally run by collegial-style management. This collegium enjoys significant legitimacy with members appointed from the legislative body. In the case of Georgia, such a body is the Board of the National Bank, whose members are nominated by the President and elected by the majority of the full composition of Parliament for a 7-year term. However, despite constitutional passage, since 2008, the supreme body of the National Bank has mostly oversight authority whereas decisions with respect to monetary and prudential policy are made single-handedly by the President of the National Bank.

A necessary hallmark for a body vested with such a broad power is independence from fiscal authorities and a high level of respectability and credibility of its own. The latter depends on the ex-ante and ex-post process. In particular, this includes the selection of monetary policy decision-makers and the outcomes of their decisions.

The ex-ante process involves staffing the National Bank's supreme body – the Board of the National Bank – and electing the President of the Bank. In this regard, the situation is less promising since the process does not warrant trust owing to its lack of transparency and several other issues. Currently, the National Bank is run by the acting President, whereas there are two vacant positions on the Board of 9 people. The President called for potential candidates to fill these positions, and eight contenders were selected for the interviews. However, their identities and interview process are closed to the public (except for two individuals noticed by the media at the entrance of the Presidential Administration). Even more harmful decisions preceded all these. For instance, the Parliament's hastily adopted amendments to the law meant adding a new position – the first vice-president of the National Bank. The President of Georgia vetoed this initiative, and the Parliament did not overcome it. This veto was not the first case between President Salome Zurabishvili and the Parliament of Georgia over the National Bank. The Parliament voted down two candidates nominated by President Zurabishvili for the Board members. After that, Deputy Minister of Economy and Deputy Minister of Finance Ekaterine Mikabadze and Nikoloz Gagua ended up on the Board of the National Bank and the former Minister of the Economy, Natia Turnava, also joined them later.

The second ex-post process is more critical for a Central Bank to retain credibility. Academic literature underscores the outcomes of monetary policy decisions (Bordo & Siklos, 2015). Furthermore, Alan Blinder suggests the definition concerning the outcome of the credibility of a Central Bank: "A central bank is credible if people believe it will do what it says" (Blinder, 2000. p.1422). Credibility for future actions stems from the past. In this case, Central Bank's future promise is to ensure inflation at a target level. In particular, it keeps inflation at a pre-determined level for a medium-term period. Since 2018, such a target figure for inflation has been 3.0%. Therefore, the credibility of the National Bank hinges on how actual inflation deviates from this figure which is also underlined by central bank economists (Tvalodze et al., 2016).

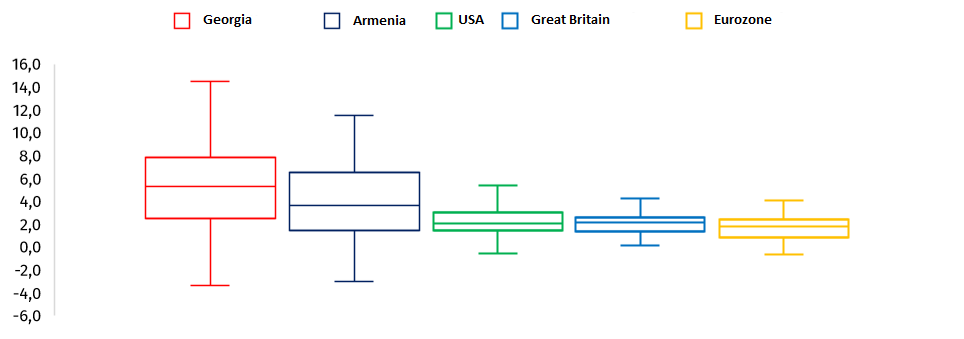

Chart 1: Annual Inflation, Box Plot: Last Two Decades (%)

Source: Central Banks; Author's Calculations

The situation in Georgia in terms of inflation is not promising because the annual growth rate of the consumer price index has been sharply exceeding the target figure for a long time. Georgia's average annual inflation over the last 20 years is 5.6% (standard deviation 4.1). In the same period, the average annual inflation in Armenia is 4.2%. Armenia is more or less comparable to Georgia, considering similar historical experience, size and economic structure. Although Armenia's inflation rate is lower than Georgia's in the long term, it is also characterised by strong fluctuations. It is possible that 2016-2020 was an exception when Armenia's annual average inflation was 1.0%, whereas, in Georgia, it was 4.2%.

Regarding the developed economies, the state of the developed economies over the last two decades has been substantially different as their inflation rates are lower. For the last 20 years, the average annual inflation in the USA was 2.5%, whereas, in the UK, it stood at 2.4%. The inflation rate in the Eurozone is much lower and stands at 1.9% on average. Of note is that in the abovementioned economic entities, the target inflation level is 2.0%, and unlike Georgia, deviation from that figure is less in scale and duration. Comparing Georgia's inflation dynamic to these countries perfectly illustrates how high Georgia's inflation rate is and the fluctuation of the latter.

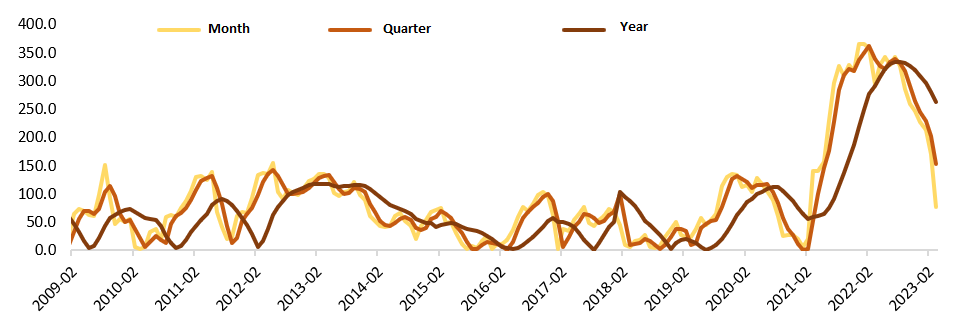

Chart 2: Deviation of Georgia's Annual Inflation from Target Level (%)

Source: National Bank of Georgia; Author's Calculations

The inflation targeting regime in Georgia has been introduced since 2009. From that period, the actual inflation rate broadly does not match a targeted level, and deviations tend to be sharp. For instance, in one month, the inflation rate deviated by 94.2% from a targeted level of 92.5% in the medium term and 80.7% on average in one year. The average deviation rate of inflation from the targeted level has been higher. At the same time, the situation in the current period has worsened. In the first half since introducing the inflation targeting regime, the average deviation from a targeted level was 64.0% in one year of annual inflation. In the second half, it was 78.2% on average. The situation in Armenia is relatively better in this regard. From 2009 until today, Armenia's annual inflation in one year deviated by 58.9% on average from a targeted level. Compared to Georgia, inflation in Armenia was more often below a targeted level.

Given previous inflation rates and strong fluctuation, the National Bank cannot have credibility. High levels of inflation and fluctuation are damaging to the economy (Fischer, 1993; Bruno & Easterly, 1995; Judson & Orphanides, 1996; Sarel, 1996; Faria & Carneiro, 2001; Grier et al., 2004; Hodge, 2006; Wilson, 2006; Munir et al., 2009; Bick, 2010; Kremer et al., 2013; Su, 2015; Mandeya & Ho, 2021), whose primary channel is investments. Under a monetary policy that lacks credibility, return on investments becomes increasingly less predictable (Dixon, 2022). Investment, as such, is considered an essential factor for long-term economic growth (Solow, 1956).

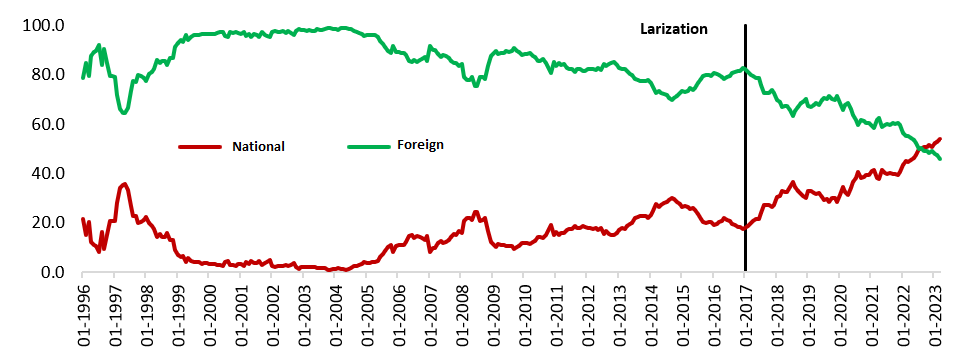

Chart 3: Composition of Term Deposit Balances in Terms of Currencies (%)

Source: National Bank of Georgia

The composition of deposits best illustrates credibility vis-à-vis the National Bank. This shows to what extent individuals and firms expect that a central bank will deliver a promise to ensure a low and stable inflation rate. Economic agents prefer to make savings in a currency whose emitter central bank enjoys higher credibility. The National Bank of Georgia is not normally considered among such central banks because the share of deposits in foreign currency is much higher. This indicates that individuals and firms do not expect the National Bank to keep Lari's purchasing power at a manifested level.

Since the introduction of the Lari until the war in 2008, the share of the national currency in the balances of term deposits was 9.7% on average which increased to 18.7% in 2017. It is true that since 2017, the share of Lari in deposits has increased, but it is an outcome of the National Bank's hard intervention – manifested in Larization. Among other things, the most rigid measure was changed to minimal reserve requirements. In particular, the reserve threshold in foreign currency increased from 15.0% to 25.0%, whereas in the national currency, it decreased from 10.0% to 5.0%. Naturally, this was reflected in the composition of deposits because such a change would reduce the incentive of commercial banks to attract foreign currency resources. In contrast, it increased the incentive of the National Bank (interest rate on deposits in the national currency increased and in foreign currency decreased).

Ultimately, to ensure low and stable inflation and safeguard a central bank's credibility, relevant institutional frameworks and rules are necessary (Kydland & Prescott, 1977; Barro & Gordon, 1983; Moser, 1999). However, in the case of the National Bank of Georgia, there is a lack of these features. On the one hand, the National Bank's current organisation (the President of the Bank single-handedly makes decisions) does not satisfy these criteria, and the Board staffing process also lacks transparency. On the other hand, monetary policy is not rules-based and disciplined. The price of lack of both is a high inflation rate and loss of economic growth.

See the attached file for the entire document with relevant sources, links and explanations.